THE ELEPHANT IS BACK IN THE ROOM

2024 was described as the biggest exercise in democracy with 40% of the global population heading to the polls. Those exercising their constitutional rights voted decisively for change with incumbents losing from Paris to Washington. While markets tend to be more concerned with profits than politics, Donald Trump’s return to the White House may prove different. His programme of deregulation and tax cuts should be better for the economy than the previous administration’s policies, but mooted changes to tariffs and immigration threaten to impact growth and inflation within and beyond US borders.

With a Republican clean sweep and an ideologically supportive Supreme Court, the scope for Trump to implement his agenda is high. The ramifications will depend on where rhetoric intersects with reality.

Equity markets had a reasonable final quarter to close out a second consecutive year of strong gains. As widely noted, US stocks led with the largest technology companies again responsible for much of the market’s stellar performance. ‘US exceptional ism’ is real – the country is outgrowing most economies globally and is home to the world’s largest and most innovative companies – but is also increasingly reflected in the region’s high valuations. With US and global equity indices increasingly concentrated, we think there is growing risk in simply ‘owning’ the index.

The global economic outlook remains supportive, with the chances of US recession appearing quite low given the strength in corporate profits, strong labour markets and supportive fiscal backdrop. Still, with analysts assuming double-digit earnings growth in the year ahead alongside more interest rate cuts despite still-lingering inflationary pressures, it’s fair to assume that expectations are higher than in the recent past.

The key risks remain inflation and bond yields. Having trended lower over the past two years the former is showing some signs of an unwelcome acceleration whereas the latter have marched higher into the end of 2024. Aspects of the incoming administration’s plan may put further upward pressure on both.

Q4 – TO THE VICTOR THE SPOILS

The dominant event for financial markets in the final quarter of 2024 was the re-election of Donald Trump.

The first nine months of the year had seen broad progress from equity markets across most geographical regions and industrial sectors. The US continued to lead the pack, benefitting from its stronger economic performance and its position at the vanguard of investment in Artificial Intelligence {Al). However, Asian, UK and European markets had also risen healthily as inflation and interest rate expectations moderated.

At a sector level it was a similar story. While Al remained the leading market theme given the scale of investment by the likes of Amazon and Microsoft, other industries were not far behind. The expectation of lower interest rates supported gains from industrial companies, consumer-facing businesses, financials and healthcare.

Bonds too were steady, having adjusted to the slower easing of interest rates, but stable given the fact that cuts had begun.

Trump’s decisive victory lit the touchpaper that blew this broad-based progress out of the water.

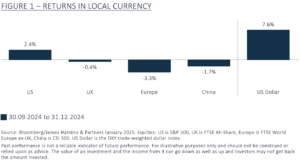

Headline moves suggest that the America First approach will be neatly mirrored in economic and market returns. Since 1st October the US market has risen whilst almost all other global indices have fallen. America’s success is coming at the expense of everyone else; most clearly encapsulated in the near 10% rise in the US dollar. Investors have voted with their wallets as US equities have benefitted from tens of billions of inflows.

With a raft of policies that may both stimulate growth and stoke inflation, expectations for interest rate cuts in 2025 receded, dragging down bonds and rate-sensitive sectors like housing, manufacturing and construction with them.

Other sector responses were equally stark, with financials rising on the prospects of deregulation whilst the healthcare sector fell by over 10% in the quarter post the announcement of Robert F Kennedy as Secretary of Health. A fitness fanatic and avowed antivaxxer, RFK has pledge to ‘Make America Healthy Again’.

Source: Fox News

Technology’s momentum has been uninterrupted by the new regime. Unlike in 2016 when global technology leaders were vocally opposed to the new President, this time CEOs have been quick to head to Mar-a-Lago to bend the knee. Jeff Bezos, Mark Zuckerberg and Sam Altman of OpenAI (which owns ChatGPT) have not only travelled to Florida to see the President but have personally pledged $1 million to Trump’s inauguration fund.

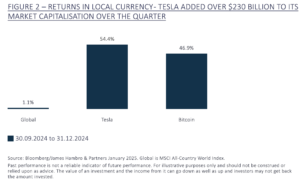

Of course, the biggest tech-bro beneficiary has been the “First Buddy” Elon Musk. The surge in Tesla’s share price adding a couple of billion dollars to his fortune.

Thus far the market response has been largely instinctive, even if it is understandable. The longer-term reality will be grounded far more in the tangible outcomes than this initial flush of sentiment.

TRUMP 2.0 – TAXES, TRADE, DEREGULATION, DEPORTATION

With the Republicans having gained control of the White House, Senate and House of Representatives there is an expectation that the administration will want to get as much as possible done before the mid-term elections in 2026. This suggests that policy will come thick and fast.

TAX

Trump likes low taxes. The Republicans have promised to extend the 2017 tax cuts on individual income that were due to expire in 2025 and there will be no increases to taxes on capital gains or inheritance. They have also floated a cut in corporate tax rates from the current level of 21% to as low as 15%. If enacted, lower taxes alone would support a 5% increase to the earnings of companies in the S&P 500.

US corporate tax rates are already amongst the lowest globally. Further reductions would provide a longer term boost to the already higher margins and earnings growth of US companies.

On the other side of the balance sheet is fiscal spending. Scott Bessent, the well-regarded nominee for Treasury Secretary, is a fiscal conservative and Elon Musk’s Department of Government Efficiency (DOGE) will be mandated to cut costs from the federal budget. Musk has been quoted as saying he will eliminate as much as $2 trillion or 30% of the federal budget. This will require cuts to social security and laying off federal employees; the scope for action looks well below the lofty ambitions. Many a businessman has been broken on the wheel of government bureaucracy.

(DE) REGULATION

Red tape is likely to be cut in a range of areas. We expect looser restrictions on financial services, merger policy and environmental regulation. Banks, energy companies and financial services businesses should all benefit. Corporate animal spirits are already evident in a brisk start to the year for mergers and acquisitions, an area likely to be unlocked by a more laissez-faire approach under the Republicans.

Deregulation should boost competitiveness, dynamism and profitability for US companies. This would contrast with the embedded biases of major competitors, most notably the EU, where Mario Draghi has highlighted the handbrake that regulation can place on innovation. The regulatory playing field is getting less level and and should favour US companies and the US dollar in general. We are intrigued by the recent behaviour of big business. The six biggest banks in the US have recently chosen to quit the global banking industry’s biggest climate group whilst Amazon and Meta are openly dialling back their diversity, equity and inclusion policies. The new regime is already changing corporate behaviour.

IMMIGRATION

Immigration was a flashpoint issue of the campaign. Trump has promised to deport millions of undocumented workers. There are currently estimated to be 11 million such immigrants in the US.

While there are of course legal and practical challenges, political reality suggests that at the very least the elevated levels of immigration of the post-Covid years will not persist.

The economic implications of reducing the size of the labour force are relatively straightforward. Fewer workers points to lower consumption and lower taxes. Combined with a trade policy promoting onshoring of domestic manufacturing and jobs, it also has the potential to increase pressure on employment and with it wages, particularly in lower-skilled jobs.

Immigration has had a positive impact on growth over America’s history. More recently, analysts have credited immigration with allowing the US to grow its economy above trend in recent years, whilst keeping wage demands sufficiently under control to allow inflation to fall.

A reversal in all types of immigration is likely to dampen the US economy’s growth potential and could add to existing pressures on both the deficit and inflation.

TARRIFS

“It’s escalate to de-escalate” – Scott Bessent, US Treasury Secretary nominee.

Tariffs were a feature of Trump’s first term and the 2024 campaign promised a blanket 20% tariff on all imports and a 60% tariff on goods from China. The proposed tariffs would raise revenue but not enough to offset tax cuts elsewhere.

Scott Bessent believes that tariffs are a policy tool that can be used to extract concessions rather than a philosophical priority. The pre inauguration shot across the bows of Canada and Mexico would align with that view, although there is likely to be some grounding.

Trump has stated that he wants to revitalise US manufacturing; protectionism looks a core pillar to success and should spur domestic investment. The trend to reshoring and the building of domestic resilience alongside infrastructure renewal was already in train, tariffs would simply provide further impetus.

There will be winners and losers at an industry level but ultimately protectionism creates friction and slows global growth for all. It will take time for supply chains to adjust to any new rules, with some companies choosing to pass either part or all tariffs on to their end consumers, while others will be forced to absorb it into their own profit margins. In the same way that tax cuts should be good for growth, so tariff increases are likely to prove a drag.

Blanket tariffs also risk a secondary impact on inflation. With consumers already scarred by rises in the cost of living any sudden increase in goods prices could be perceived as another wave of price pressures and subsequently find their way into inflationary expectations and wage demands.

Trump may not have it all his own way. Despite its struggles China has not sat on its hands since 2016. It has invested substantially in its domestic industrial capabilities and may be more willing to fight back against US tariffs. Its recent response to another round of US restrictions on technology was to limit the export of some lesser-known minerals key to the battery and renewable energy markets; one reason behind the sudden interest in Greenland. With Apple, Nvidia and Tesla all having major operations and sales in China, the trade war may not be as easy for the China hawks in the administration to win this time, at least not without domestic casualties.

BOTTOM LINE

The billion-dollar question is where the policy reality will intersect with the election rhetoric. This will only become clear in the months following 20th January.

Much may depend upon the order in which policies are enacted. With growth expectations higher for this year, markets are more vulnerable to disappointment.

OUTLOOK FOR MARKETS – A HIGHER HURDLE

INTEREST RATES BONDS AND INFLATION

“I feel like an MMA fighter who keeps getting inflation in a choke hold, waiting for it to tap out yet it keeps slipping out of my grasp at the last minute. But let me assure you that submission is inevitable — inflation isn’t getting out of the octagon.” – Fed Governor, Christopher Waller.

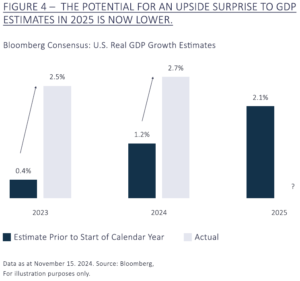

The continued strength of the US economy has forced the Federal Reserve (Fed) to raise their inflationary forecasts and reduce their expectations for rate cuts. The Fed is still talking tough on inflation and rate rises in the US this year are not completely off the table.

Whilst we think that inflation will prove to be more of a feature of economies than it has been for more than a decade, bond markets are likely to spend much of this year as much focussed on fiscal policy as the monetary decisions made by central banks.

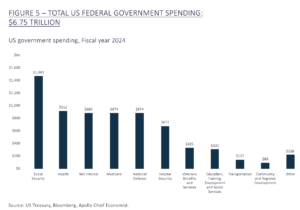

Deficits have been on the rise with the US running an annual deficit of 6% of GDP whilst US debt to GDP has increased from 100% to 120% in the last five years. Net interest on outstanding debt is now costing the US nearly $900 billion per annum, making it the third largest outlay of the Federal Government, more than either Defense or Medicare.

Alongside a more mercurial administration, that has previously questioned whether the Fed should remain independent, further expansions in the deficit creates the potential for mischief at the longer-dated end of the bond market. Ten-year US treasury bond yields have risen in the last three months even as rates have been cut.

The UK faces some of the same issues, although sticky inflation is less a result of robust growth than the UK’s vulnerability to price volatility given the greater reliance on imported goods. The potential impact of fiscal spending on the UK deficit has also exerted upward pressure on bond yields. If confidence in the government’s policies deteriorate further, we could see more upheaval in the UK government bond (gilt) market. The spectre of the Truss government’s economic chaos still looms large.

With yields of over 4%, UK and US government bonds are still much more attractive than for much of the last decade and should protect value in the event of recession. Given our view of bonds as protective investments with low levels of volatility we prefer to hold shorter-dated bonds.

EQUITIES – BIFURCATION

Global equity markets are coming off the back of another strong year in 2024. Again, the leading light was the US and within it the Al-centric technology businessses. For the second year running the ‘Magnificent largest 7’ technology companies represented around 50% of the US market return.

Will 2025 represent a “threepeat” for the US and Al or will we see an overdue broadening out of growth and returns to other areas supported by US economic strength and the wider industrial manufacturing sector emerging from a two year slump?

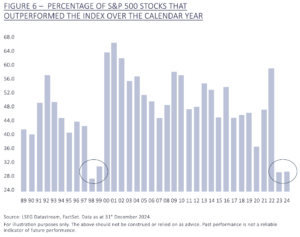

The breadth of performance across global and particularly US equity markets has been very poor over the past two years, with the only recent analogue being the exceptionally narrow market in the late 1990s dot-com bubble.

Headline valuations for global markets look rich versus history but reflect the dominating influence of an expensive US market that now accounts for almost 70% of the value of the global equity market index. The rest of the world looks unremarkable compared to averages over the last thirty years.

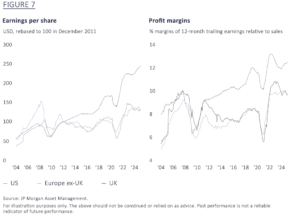

Within the US headline equity valuations are unquestionably high, even removing the impact of the technology behemoths, but they are still below both the 2021 and 2000 peaks. The US market is a higher quality index than it was back then; margins are higher, capital intensity lower and balance sheet leverage is reduced. It is also manifestly higher quality than European and UK indices. Earnings and profit margins have been stronger as has the pace of corporate innovation as US companies have benefitted from lower tax and less regulation – an advantage that should be cemented under Trump.

Valuation alone is not a reason to turn negative and whilst earnings continue to grow and given a supportive macro backdrop we would expect further progress. It does, however, leave the market more vulnerable to swings in sentiment which points to higher volatility and bouts of weakness ahead.

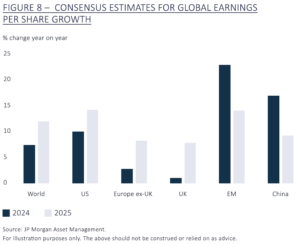

Corporate earnings are expected to accelerate in 2025, with the US continuing to lead but by a lesser margin. US earnings are forecast to rise by nearly 14% this year and global earnings by 12%, the fundamental backdrop should support another year of gains.

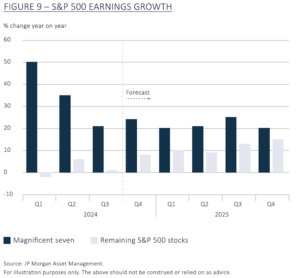

Gains should come from a much wider group of companies than technology as the economic resurgence is felt by an ever-wider proportion of businesses in different industries.

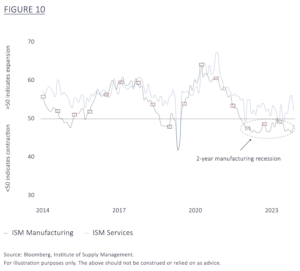

Manufacturing has been in a two-year recession as the aftermath of Covid supply chain chaos collided with higher rates, a collapse in China and stagnation in Europe. Pressures are beginning to ease; the US continues to be in industrial and manufacturing renewal and the incoming administration is flagrantly in favour of bringing manufacturing home.

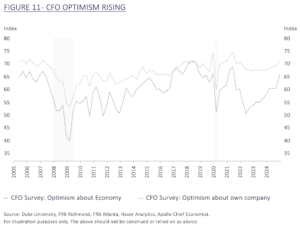

We have invested in several companies that have been holding their own despite this slowdown. The recovery to normalised levels of demand post the pandemic has taken longer than most expected, but the companies in which we are invested have a history of getting leaner and fitter in downturns and so should be well placed for both an inflection in earnings but also any change in investor priorities. With corporate optimism on the rise this could be soon.

It is impossible to ignore Al given the media ubiquity, investor hyperbole and capital outlay. The money is real, and the beneficiaries are seeing big orders for chips and data centres. The Magnificent Seven account for 35% of the S&P 500, have generated 70% of the market return since 2023 and now trade on a 50% premium valuation to the market.

With US and global equity indices increasingly concentrated, we think there is growing risk in simply ‘owning’ the index. While the trends of the past few years may continue, our more diversified exposures are intended to position portfolios to benefit across a far wider range of scenarios. As we have said before we believe it is more prudent to prepare for an uncertain future rather than predict it.

GOLD – THE ONLY ALTERNATIVE TO THE DOLLAR?

Gold has continued to benefit from shifting strategic priorities of governments and central banks, outperforming all major asset classes in 2024. Historically gold has tended to lag during periods where equity markets, the dollar and economies have been strong, so 2024 is something of an outlier.

Gold is benefitting from a concerted effort by many nations to reduce their reliance on the dollar and vulnerability to US sanctions. China, India, Russia, Turkey and others continue to reduce their holdings of US treasuries having increasingly seen the risks of being beholden to US policy.

Gold has shown an ability to be a rewarding asset in both benign and challenging markets and its safe haven credentials were burnished both during Covid and the early weeks of the invasion of Ukraine.

With geopolitical risks unlikely to abate, inflation down but by no means out and central banks continuing to reduce their reliance on US Treasuries and the dollar, gold’s credentials as a diversifying asset are still valuable.

CONCLUSION

Equity bear markets rarely occur without either a hike in interest rates or a recession. There are few signs of either happening in the early part of the year.

The interest rate cycle turned decisively last year with interest rates falling across the US, Europe, UK and China. The fact that inflation is still above target remains a pea under the mattress for central banks, but they are still signalling that rates will fall, albeit maybe not as quickly as markets had hoped.

Stubborn inflation in the US is a consequence of the resolute strength of the US economy, which continues to exceed expectations. Government support, Al spend and a recovery in productivity have all propelled growth. The trade off between growth and inflation may become more nuanced if it keeps interest rates at current levels but growth is ultimately good for companies and their profits.

The incoming Trump administration has stated its purpose is to at the very least perpetuate US hegemony whilst stoking the fire of the US’s industrial and manufacturing renewal. This will support the broadening out of corporate performance beyond technology.

Article written by James Beck, Partner, Head of Investments

This document is a Financial Promotion for UK regulatory purposes and is directed only at investors resident in the United Kingdom.

This document does not constitute investment advice or a recommendation.

Past performance is not a reliable indicator of future performance. The value of investments, and the income from them, may go down as well as up, so you could get back less than you invested.

This material has been issued and approved in the UK by James Hambro & Partners LLP, which is authorised and regulated by the Financial Conduct Authority and is a registered investment adviser of the Securities and Exchange Commission. It is listed in the Financial Services Register with reference number 513246. James Hambro & Partners LLP is a limited liability partnership registered in England & Wales with number OC350134 and registered office at 45 Pall Mall, London SWl Y 5JG. A list of members is available on request. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence.