NEW WORLD ORDER

The fallout from the extraordinary set of tariffs introduced by President Trump on 2nd April will continue to dominate the immediate market environment. The initially proposed rates have the potential to push the global economy into an unnecessary recession. The good news is that, unlike previous crises, there are no major structural imbalances in the economy and consumers in aggregate entered the year in a position of strength. The recent sell-off was self-induced and can be rectified by changing policy.

Near-term uncertainty aside, longer-term trends are clear. In this note we explore some of those developments and find good grounds for optimism.

We have previously written about how structural changes since the pandemic suggest a different economic and investing environment in the years ahead. Less than 100 days into his second stint in the White House, President Trump has accelerated these shifts.

Fiscal spending has regained prominence as governments have moved to prioritise economic resilience over optimisation. Strategic industrial policy has returned with trade increasingly flowing along political rather than economic lines.

Private investment is following public, as companies reorganise supply chains and battle for Artificial Intelligence (Al} leadership. Persistent labour shortages and higher wages are creating a stronger incentive to invest in new technologies and work existing resources harder. These forces will drive more capital investment and faster economic growth.

The inflation regime is also shifting. In a globalising world, with supply plentiful, changes in demand were the predominant influence on prices, and could be supported or subdued through an expanding central bank toolbox. In a less open economic climate, domestic inflation will increasingly be dictated by supply shocks that are less neatly addressed by changes in interest rates. Inflation is more likely to drift too high than slip too low, with monetary policy needing to be more sledgehammer and less scalpel.

This is not necessarily a ‘bad’ environment for investing. Medium-term growth prospects have improved compared with the lacklustre conditions of the 2010s. But this new world order will be marked by shorter, more volatile economic cycles and a less reliable relationship between asset classes and stock market leaders.

The set-and-forget portfolios of the past may be the wrong approach for the future. After a decade in the wilderness, conditions look set for a long-awaited renaissance in active investment management.

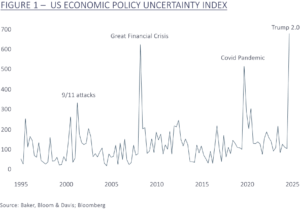

A BULL MARKET IN UNCERTAINTY

Investors have come to the realisation that trade tariffs are less bluff and more policy. Yet as with many Trump pronouncements, the relationship between what the President says and what ultimately happens is highly erratic.

The seat-of-your-pants policy approach has left executives and investors confused at best, fearful at worst. Questions through the start of the year included the basic (what will tariff rates be, on what goods and against whom?), the complicated (how will trading partners retaliate, how will the affected accompanies adjust prices and how easily can US consumers switch to tariff-free substitutes?) and the unknowable (to what extent are tariffs a temporary negotiating tool as opposed to a permanent revenue raiser?).

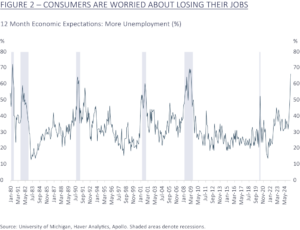

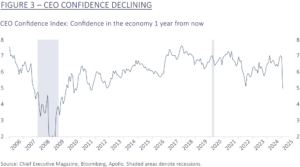

No wonder consumer and corporate confidence has nose-dived.

Trump’s trade war has the potential to bring on a recession should it broaden dramatically. At face value, the menu of rates unveiled on 2nd April in the White House rose garden were even worse than feared. Few suspected a 10% blanket charge on all imports plus severe ‘reciprocal’ rates on major trading partners such as China (54% tariff rate which has since risen to over 100%), Japan (24%) and the EU (20%).

While the negative equity and bond market reaction may have convinced Trump to introduce a 90 day stay of execution for most, if the policy is enacted unchanged the average effective US tariff rate would jump to over 20%. This would be the highest in over a century.

The US Administration is turning out to be more ideological than first assumed, with the associated policy uncertainty encouraging companies to delay hiring and investment decisions and consumers to pull back on spending. If this leads to a sustained deterioration in demand, companies may respond by cutting their headcount, setting off a classic recessionary dynamic: job losses leading to reduced confidence and spending, lower corporate revenues and further redundancy rounds. Although we expect actual implemented tariffs to decrease as countries negotiate bilateral deals, should higher rates remain in place the impact on growth and inflation will be significant.

While recession risk is building, the underlying strength of the US economy means it is by no means certain. Consumers in aggregate remain in rude financial health, the Federal Reserve has room to reduce interest rates and the direct impact of tariffs should only be modest. Trade and manufacturing are small components of the services-driven US economy and imported consumer goods represent less than 5% of private consumption spending in the US.

There is also the real political risk that an avoidable slowdown is brought on by a policy most Americans care little about (Fig. 5), raising the odds of a trademark Trump course-correction should the economy or his approval ratings begin to sour. A self inflicted, inflationary recession would be disastrous for Republican prospects at the mid-term elections next year and their ability to achieve their longer-term goals.

While tariff levels will likely remain a moving target, the relative impact of each announcement should lessen, particularly if the Administration pivots towards the more market-friendly aspects of its policy agenda like deregulation and tax cuts.

However, more meaningful for long-term investors is the evidence that Trump is accelerating the transition from monetary-policy dominance to fiscal-policy prominence. This has significant investment implications.

THE RETURN OF STRATEGIC INDUSTRIAL POLICY

Control of economic policy is being wrestled away from central bankers and returned to politicians.

The transition has been gradual and has been in response to the general view that low interest rates and globalisation have not benefited everyone.

Although likely a more pro-growth policy mix than seen over the last decade, the downside of having governments in the driving seat is a more unpredictable decision-making process. If interest rate changes can act on the economy in mysterious ways (the oft-quoted ‘long and variable lags’), they are surgical in comparison to fiscal policy. When taxes or spending are raised or lowered it is not always clear when, where, on whom and by how much the impact will be felt.

Politicians also can’t be relied on to make rational economic choices. Instead, their policies are designed to favour their voters and re-election prospects. These decisions take time, are harder to predict (and invest against) and on balance tend to produce a more inflationary environment than a monetary policy dominated regime. With central bankers relegated to a reactive rather than proactive role, you have the ingredients needed to deliver a more volatile economic environment.

FROM MAGA TO MEGA. MAKE EUROPE GREAT AGAIN

The passing of the baton from monetary to fiscal policymakers is not just a US phenomenon.

Stepping into 2025, investor expectations for Europe were depressed with good reason. Over-regulated and bureaucratic, with a lethargic economy lacking a technology sector of real heft, it is also held back by rising geopolitical risk and an ageing population. Most expected a continuation of ‘US exceptionalism’ and big-tech outperformance; the dominant market story of the past few years.

Yet an increasingly chaotic US policy agenda combined with signs that American hostility will encourage Europe to stimulate its economy have driven a reversal of fortunes.

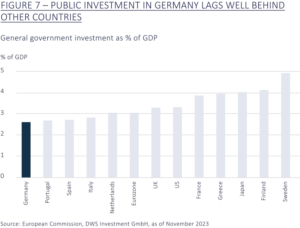

In an historic move in March, traditionally debt-shy German lawmakers voted to allow a huge increase in spending. The move frees up a much-needed €500bn for German infrastructure (Fig. 7) while exempting spending on defence from Germany’s strict debt rules. Separately, Europe’s defence spending plan, ReARM Europe, is worth an additional €800bn of potential spending, or around 0.5% of the region’s GDP annually.

With the ‘US exceptionalism’ narrative under a cloud for now, European markets have benefited. The Euro Stoxx index of the continent’s 50 leading blue chips rose by 12% in the first quarter against the S&P 500 which fell by 4%, Europe’s second largest quarter of outperformance relative to the US this century.

While much of this move represents an unwinding of investor positioning, the region’s shift towards expansive fiscal policy introduces a growth catalyst that Europe has lacked for over a decade. This could be a seismic shift for European equity earnings and valuations.

As well as providing a host of high-wage manufacturing roles, defence spending has a well-proven history of spurring innovation and productivity improvements that go well beyond the battlefield. Breakthrough technologies from radar and jet engines to semiconductors and the internet all find their roots in defence sector R&D.

Europe has also disproportionately suffered from a combination of forces that have amplified America’s relative advantage since the pandemic. US energy independence and more generous fiscal handouts helped prevent the cost-of-living crisis seen across Europe as energy bills rocketed in the aftermath of the Russia- Ukraine war. A rolling two-year manufacturing recession alongside China’s refusal to stimulate its economy hurt the more industrial and export focused economies across the continent, while the service-led US economy was comparatively immune. As interest rates rose in tandem across much of the world, 30-year fixed rate mortgages protected US homeowners whilst Europeans were squeezed by higher borrowing costs as shorter-term loans repriced higher.

The good news is that these forces are now easing. Wages are outpacing prices, manufacturers have worked off excess inventories and central banks plan to continue easing policy which should provide relief to those struggling most from higher rates. China too has shown a willingness to unleash economic stimulus and a potential ceasefire in Ukraine would bring a welcome reduction in energy costs.

After a decade of American dominance, we are optimistic that some of our European companies may enjoy brighter times ahead.

UNDER PRESSURE

Perhaps the biggest economic difference today versus the 2010s is the health of the labour market. Most economies are operating at or near full employment and the Euro area has its strongest labour market in decades.

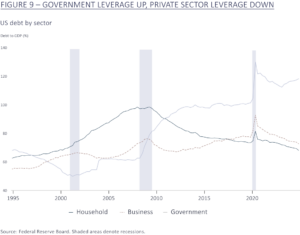

The persistently weak job markets of the 2010s depressed wages, discouraged investment and constrained productivity. Tighter labour markets should drive the reverse. After more than a decade of deleveraging, consumer balance sheets are strong (Fig. 9), setting the stage for a revival in credit growth, a typical support to economic expansions in the past.

Combined with a more pro-growth policy mix, the resulting ‘higher-pressure’ global economy is stronger and more balanced today than during the pre-pandemic period.

INFLATION AND INVESTMENT CONSEQUENCES – ACTIVE RENAISSANCE?

Fiscal prominence, deglobalisation and tighter labour markets will also alter the nature of inflation, shifting it from being driven by demand, with supply virtually unconstrained, to being dominated once again by supply-side shocks.

Why does this matter?

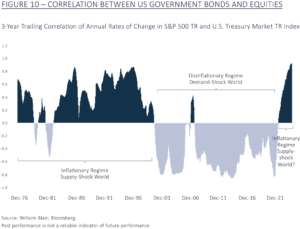

For most of the 21st century, investors have enjoyed the diversification ‘free lunch’ enabled by a consistent negative correlation between bonds and equities. When markets swooned, bonds swelled, providing effective protection for the typical balanced investor.

Helped by the introduction of China into the World Trade Organisation in 2001, a globalised world of outsourced supply chains delivered a quick response to supply shortfalls. Perma-lukewarm labour markets after the financial crisis plus the ability to offshore production to low-cost countries meant little bargaining power for workers. With little upside risk from inflation, the framework for any self-respecting central banker was to lower interest rates at any sign of trouble.

The investment playbook became equally clear. Low rates, tepid economic progress and a 2% inflation rate that felt like a ceiling rather than target encouraged buy-and-hold investment in those few areas that could deliver growth. Momentum rather than valuation became the greater predictor of returns, leading to ever-more concentrated equity markets. Firm in the knowledge that central bankers would take care of any bumps in the road, bonds, with their negative correlation to equities, were all the diversification required.

In short, the archetypal 60:40 balanced portfolio (60% equities: 40% government bonds) was all one needed. While this environment made fundamental value-driven investment less relevant, it created the perfect backdrop for the success of passive investment.

The move to a world where inflation is driven by changes in supply has major implications. Tariffs, labour shortages and geopolitical fallouts have a nasty habit of both weighing on growth (bad for equities) and raising inflation (bad for bonds). As shown in 2022, bonds may not always prove a reliable hedge.

A supply-driven regime need not mean permanently high inflation, but it will tend to drift too high rather than fall too low, and the overall volatility of price changes is likely to increase.

By extension, this suggests a return to more dynamic interest rate cycles, greater swings in GDP growth, shorter economic cycles and more rapid shifts in stock market leadership than the pre-pandemic decade.

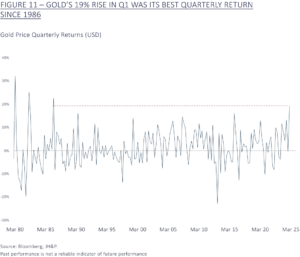

Portfolios may need to be more dynamic and will likely benefit from broader diversification across and within asset classes. Unable to rely solely on bonds for portfolio insurance needs, investors will need to look to a wider range of equity sectors and investment classes to construct resilient portfolios for an uncertain new world. It is perhaps instructive that gold has just posted its best quarterly return in almost 40 years (Fig. 11).

Finally, the return of higher interest rates, economic uncertainty and unreliable relationships between asset classes will result in a renewed focus on valuation within the investment process.

After a decade of strong performance, US and global equity markets are characterised by higher valuations and greater concentration than at any point since the internet bubble at the turn of the century. The world is changing; portfolios may need to change too.

A BRIGHTER FUTURE?

Frenzied policy is damaging confidence while Elon Musk’s DOGE government purge may weaken the currently resilient US labour market. Though the Federal Reserve has room to cut rates, the likely inflationary impulse from new trade barriers leaves them reticent to move too quickly. The US can still avoid a recession this year, but the risks have clearly increased.

Market upheaval inevitably leads to shortening investor time horizons. While every drawdown is unsettling, they are not unusual – a market fall of 10% or more happens about every two years. This is why we construct balanced portfolios with a focus on companies whose operating performance is resilient through different environments. These high-quality businesses have a long history of adapting to political and economic change and tend to emerge from challenging trading conditions with an even greater advantage over competitors. Many also now have considerably more valuation appeal for the longer-term investor. We will continue to adjust portfolios to take advantage.

If the short-term path now looks less than certain, the longer-term destination is increasingly clear.

We may at last have stumbled upon a faster growth and more reflationary environment than that of the deflationary decade after the global financial crisis. This is good news.

Whilst this new environment means inflation will be higher on average than the previous decade, it should also drive higher wages and labour participation rates, greater corporate investment and faster productivity growth, and a reduction in inequality more generally. More dynamic interest rate cycles, shifts in stock market leadership and a less reliable relationship between asset classes will demand a more diversified and active approach than the set-and forget portfolios of the recent past.

Who knows, it may eventually lead to less toxic politics.

Article written by Dan Zegleman, Portfolio Manager.

This document is a Financial Promotion for UK regulatory purposes and is directed only at investors resident in the United Kingdom.

This document does not constitute investment advice or a recommendation.

Past performance is not a reliable indicator of future performance. The value of investments, and the income from them, may go down as well as up, so you could get back less than you invested.

This material has been issued and approved in the UK by James Hambro & Partners LLP, which is authorised and regulated by the Financial Conduct Authority and is a registered investment adviser of the Securities and Exchange Commission. It is listed in the Financial Services Register with reference number 513246. James Hambro & Partners LLP is a limited liability partnership registered in England & Wales with number OC350134 and registered office at 45 Pall Mall, London SWl Y 5JG. A list of members is available on request. The registered mark James Hambro® is the property of Mr J D Hambro and is used under licence.